Transparency International ( New Zealand) has recently undertaken a national integrity survey.

Transparency International ( New Zealand) has recently undertaken a national integrity survey.

A quick look at their web site http://www.transparency.org.nz/ flashes up messages such as” Least corrupt public sector in the world “.“New Zealand’s high trust public sector is its greatest competitive advantage”

The integrity survey cost $174,320 , the accounts do not reveal who the recipients of that payment was but I do believe that a sizable chunk of it went to the chair person Susan Snively .

the survey was funded in the following manner

Income

National Integrity Systems Assessment

Donation: Gama Foundation $15,000

Office of the Auditor General $30.000

The Treasury $30.000

Ministry of Justice $30.000

Statistics New Zealand $15.000

States Services Commission $10.000

Ministry of Social Development $10.000

Other $55.000

now look at the pillars of the integrity system they are

Legislature (pillar 1)

Political executive – Cabinet (pillar 2)

Judiciary (pillar 3)

Public sector (pillar 4)

Law enforcement and anti-corruption agencies (pillars 5 and 9)

Electoral management body (pillar 6)

Ombudsman (pillar 7)

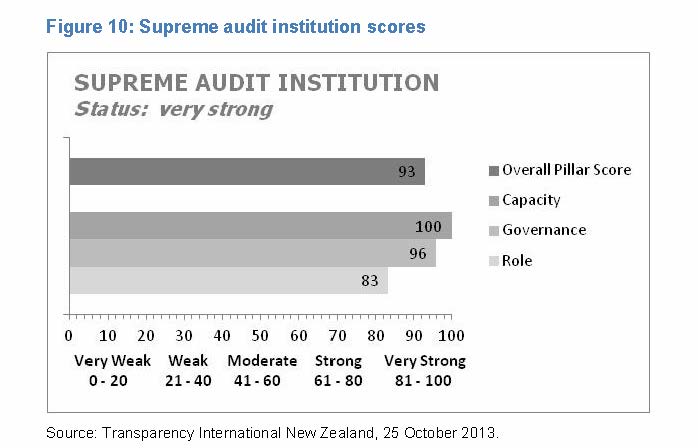

Supreme audit institution (pillar 8)

Political parties (pillar 10)

Media (pillar 11)

Civil society (pillar 12)

Business (pillar 13)

looking in particular at the Supreme audit institution you will note that the $15,000 donation in 2012 and the $30,000 donation 2013 have not been wasted.

When you see high scores like that you could be mistaken in thinking that this is the reality . The reality is that Here in New Zealand we are very good at manipulating data .

Three pages worth looking at at the auditor generals we site

how fraud was detected , Fraud types and methods of committing fraud

Fist of all How fraud was detected

Internal control systems were deemed to be the most effective method of detecting fraud . This is best assessed in conjunction with the Price Water House coopers publication prepared on behalf of the auditor general page 85 is particularly interesting in that it shows a very low percentage of entities having a whistle-blowers hotline.

But internationally Whistleblowers are Still the Best at Detecting Fraud.

It is no surprise that this is not the case in New Zealand as the systems are not in place for whistle blowers according to the auditor generals own figures .

What I notice here is that all the frauds are $$ based. In true auditor style we need figures. but not all frauds occur in such a way that good book keeping can pick them up – there is a very large field called Identity fraud which is not represented in the tables and I wonder if it is at all considered.

Again we have the word theft occurring repeatedly , Theft generally implies that you have something and next it is gone without your permission.

The frauds which are very prevalent in New Zealand are identity frauds perpetrated through fictitious organizations and secret trusts.

Money is moved from one entity into a seemingly legitimate trust and then the trust is split off and dissolved in a very non transparent manner

The fraud which has impacted on my life is one where a person pretended to be a trust. a fictitious trust obtained law enforcement powers and the one person carried out the duties of this fictional trust using the staff and resources of a council . This type of fraud is apparently condoned by the auditor general as shown by this correspondence.correspondence with the auditor general

The office of the auditor general claims to be Parliaments watch dog it would appear that this watch dog is asleep as the office of the auditor General in New Zealand condones fraud as follows

- 1. Making a false application to the minister 22 November 1999 this document in itself is a fraud on the government .. using a document for a pecuniary advantage. AWINZ does not exist it is not a legal person in any manner or form. condoning a criminal act.

- 2. Central government giving coercive law enforcement powers to an entity which does not exist and no one checks for its exists, even when they know it does not exist they continue to pretend that it does. condoning a criminal act.

- 3. MPI not having the slightest idea of what a trust is and how a trust should function, and allowing the false application to be justified because 6 years later they received a trust deed which was signed 3 months after the application was made. The fact that the people who had signed that deed had never met or made a valid decision between, was totally beside the point. condoning incompetence .

- 4. MAF ( now MPI) not being in possession of a trust deed with the party to whom law enforcement powers had been given and then getting a trust deed which was altered or fabricated, and ignoring this despite having this pointed out to them. Deed provide June 2006 this is the deed MAF have on file condoning incompetence .

- 5. Using fictions names for contracts to local and central government. Mou Waitakere & MOU MAF condoning a criminal act.

- 6. Council employees contracting to themselves Mou Waitakere ( Mr Wells became both parties to this contract). condoning a criminal act.

- 7. Employees obtaining employment at council without declaring a conflict of interest condoning corrupt actions .

- 8. Council manager writing to the crown consenting to the use of staff and resources to fictional third parties North shore city and Waitakere city condoning this corrupt action.

- 9. Council managers using council resources in a manner so that the premises take on a look and feel of a private enterprise , even MAf was confused as to where the fictional AWINZ finished and the council property began . condoning a criminal act.

- 10. Use of council resources to solicit donations the funds of which are then misappropriated ( you were there when I did my presentation) condoning a criminal act.

- 11. Allowing a trust set up in 2006 to pretend to be the law enforcement authority . This trust became a charity and has used its charitable funds, obtained from the public to conceal corruption condoning a criminal act.

- 12. The processes within the government department and councils are such that they serve to conceal fraud as the very persons involved and implicated for their lack of diligence are put in charge of the release of information, additionally Mr Wells was consulted on what was released to me and what was not there was no impartiality between the department/ council and third parties condoning this incompetent practice .

Why do we have to pretend to be the least corrupt why cant we deal with the reality , Corruption happens, dont condone it deal with it that will ensure that corruption does not ruin lives .

By outsourcing your services to private enterprise teh office of the auditor general has lost control over the process , but in the end its the perception that is worth preserving and that is why the office of the auditor general is a member of transparency International New Zealand , that is as good as any watch dog being a member of the local gang.

so much for the rules of independence

Leave a Reply